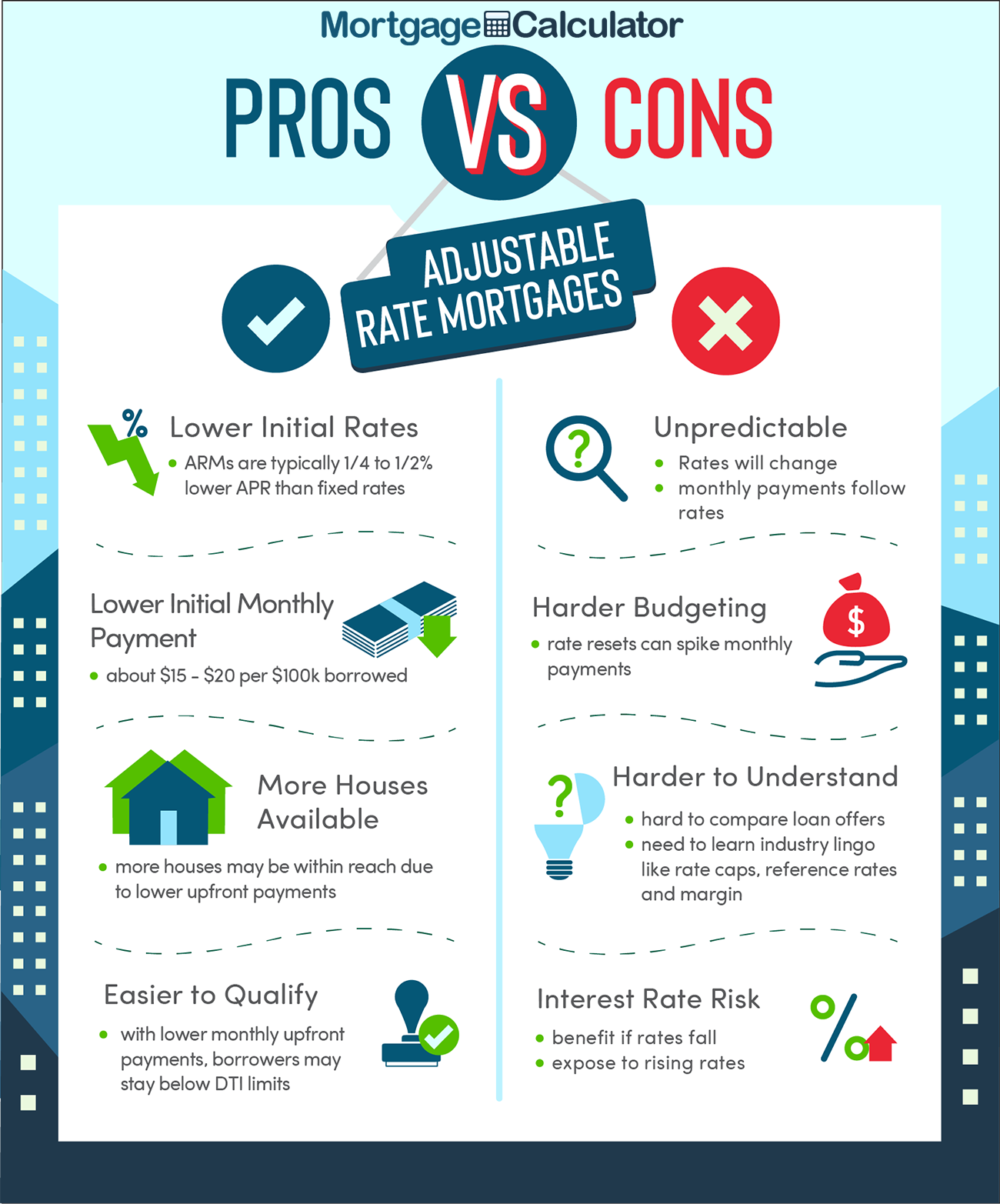

Some people believe fixed-rate home mortgages are constantly the far better option. However ARMs can be a choice for house purchasers that recognize they will certainly have the funding for only a few years, states Don Maxon, a qualified financial organizer in San Rafael, California. One method to save cash over the life of the finance when you obtain an ARM is to put the money you conserve from that reduced rate of interest back directly towards the principal. By doing this, even if the interest rate adjusts up, you're paying much less in rate of interest due to the fact that you're paying it on a lower equilibrium. To Discover more see how this works in practice, allow's have a look at the earlier scenario where we were saving $70.93 each month by selecting an ARM.

Naturally, there is constantly the danger that you won't have the ability to offer your home prior to your price changes. If that occurs, you may wish to https://sokodirectory.com/2017/07/high-gdp-annual-returns-key-supporters-growth-real-estate-sector/ take into consideration re-financing into a fixed-rate or a new flexible price home mortgage. Nevertheless, you're still running the risk that rate of interest will certainly have boosted then. See the full article for the kind of ARM that Adverse amortization financings are naturally. Higher risk items, such as First Lien Regular monthly Flexible fundings with Adverse amortization as well as Residence equity lines of credit have various means of structuring the Cap than a common First Lien Home mortgage.

- Yet in addition to other consumer supporters, she acknowledges that reforms implemented considering that the housing accident have actually helped reduce the threats of adjustable-rate lendings by needing lenders to validate a customer's repayment ability.

- If you can afford it, any type of added settlement goes straight towards the principle.

- The authors claimed lenders were distributing 2 or three-year ARM items with low first settlements that customers can re-finance out of as soon as the price matures.

- The other method to protect that 3.33 interest rate is to select a 5/1 ARM home mortgage.

- It deserves noting that ARM prices can readjust down in addition to up, depending on market problems.

The benefit for the consumer is that the month-to-month payment is guaranteed never ever to be increased, and also the lifetime of the car loan is likewise repaired ahead of time. The negative aspect is that this model, in which you have to start paying several years before really obtaining the lending, is mostly targeted at unbelievable residence purchasers that have the ability to prepare in advance for a very long time. That has actually come to be a trouble with the usually greater mobility that is required of workers nowadays. In contrast, dealt with price home loans created 15, 20, or 30 years have a set quantity of rate of interest on the lending that does not alter.

Adhere To Eye On Real Estate Using E-mail

The level of earnings you have will help the lending institution establish just how large of a home loan repayment you can receive. For example, let's say that you obtain a 30-year ARM with a 5-year set period. That would bring about a fixed price for the first 5 years of the car loan. After that, your rate could rise or down for the staying 25 years of the lending.

Key Mortgage Market Research

Consumers were typically brought about assume that residence costs would certainly continue rising, which would allow them tap into the equity they had built up and roll over their burgeoning financial obligation right into a brand-new lending. Variable-rate mortgages provide initial prices below prices for conventional home loans, that usually readjust after five to 10 years, at periods of one to 2 years. As of Friday, the interest rate for an 5/1 adjustable-rate mortgage, for example, was 4.68 percent for the initial 5 years, with yearly adjustments, contrasted to 5.64 percent for a traditional 30-year funding. The big drawback is that your monthly repayment can skyrocket if rate of interest climb. Many people are stunned when the interest rate resets, even though it's in the contract. If your revenue hasn't risen, after that you could not have the ability to afford your home any longer, and you could lose it.

If those strategies allow you to sell the initial house prior to the interest rate starts to fluctuate, after that the risks of an ARM are fairly marginal. With appealing interest rates offered, now may be a good time to consider locking in a reduced price throughout of your car loan. Given that a brand-new home loan is included, you'll require to experience a lot of the very same steps you took when looking for your initial mortgage. As an example, you'll likely need to provide pay stubs, bank statements, as Visit the website well as tax returns. Actual repayments will differ based upon your specific circumstance as well as existing price. There's a possibility your payment can go down if rate of interest fall.

For the majority of people, an ARM is not the very best option when funding a home acquisition. The chart listed below highlights the difference in ARM as well as LIBOR prices from 2005 via 2020. Doretha Clemons, Ph.D., MBA, PMP, has actually been a business IT executive and professor for 34 years. She is a complement professor at Connecticut State Colleges & Colleges, Maryville University, as well as Indiana Wesleyan College.

As an example, if you plan to sell the home before the rates of interest starts to adjust, those possible adjustments might not be an issue for your budget. For that reason, the rate and also repayment results you see from this calculator may not show your actual circumstance. You may still qualify for a loan also in your scenario doesn't match our presumptions.

The Pay

That obtains you the great old 2012 rate of interest, without offering every little thing you have on ebay.com to pay your discount rate factors. For a $300,000 mortgage, getting from 4.2 percent to 3.33 percent might cost you $18,000 to $24,000. Yet just two that do not involve the higher repayments of a 15-year home mortgage. " It will be time to stress if funding requirements begin to loosen up as well as anybody who can fog a mirror has the ability to get a home mortgage. That is not what is occurring currently."

That suggests that your month-to-month home loan repayment will remain consistent for the life of the finance. The first number shows how years the rates of interest is taken care of. The number after the reduce shows how several months the change duration is. As an example, a 5/6 ARM offers a fixed price for 5 years, then the price adjusts every 6 months. You'll need to get these finances with approved lenders instead of with the federal government firms themselves.